Unlocking trading performance in this year’s generally downward-trending market has not been easy. Whichever direction the markets have headed, the biggest daily moves have been roughly equal in terms of trading friction: the big up days have not been any simpler to trade than the big down ones. This is true whether we look at big days for the whole market, or big days for individual stocks - at least in the universe of top 1000 traders, ex-ETFs.

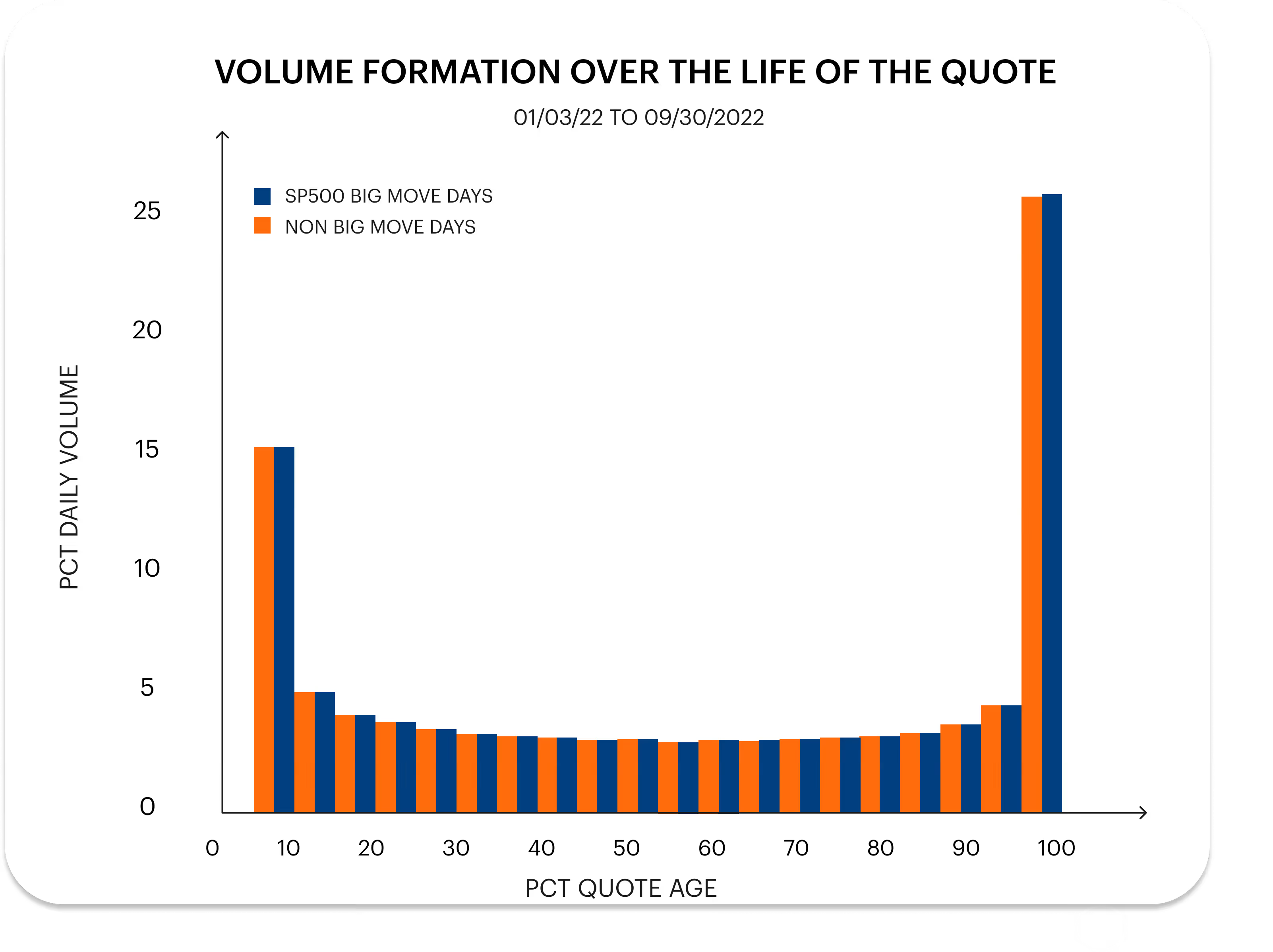

Surprisingly, how volume builds over the life of individual quotes does not shift, regardless of the magnitude or direction of the stock or market’s move. As a quote changes, there is a spike of volume that fades quickly into the middle age of a quote, followed by a large spike of volume right as the quote begins to change.

Not only does this pattern remain consistent, but the relative contribution of each stage of a quote’s life to total volume remains consistent as well. For example, come rain or shine in the market, about 30% of the day’s volume comes as the quote changes to a new level. But as quotes change, prices become more directional separating winners from losers. This accelerates on ‘big move’ days.

What's a ‘big move? Let’s define it as the top and bottom deciles of intraday returns for single stocks and overnight returns for the S&P 500 respectively. Big days are characterized by higher volumes, but these higher volumes come with the added expense of wider spreads and faster moving quotes and that leads to higher mark-outs and less post trade quote-stability.

Discrete, timed matches on IntelligentCross helps place trades during the more stable mid-life of a quote, giving subscribers time to reload or take advantage of both spread-saving intraspread or midpoint liquidity.

Unlocking trading performance in this year’s generally downward-trending market has not been easy. Whichever direction the markets have headed, the biggest daily moves have been roughly equal in terms of trading friction: the big up days have not been any simpler to trade than the big down ones. This is true whether we look at big days for the whole market, or big days for individual stocks - at least in the universe of top 1000 traders, ex-ETFs.

Surprisingly, how volume builds over the life of individual quotes does not shift, regardless of the magnitude or direction of the stock or market’s move. As a quote changes, there is a spike of volume that fades quickly into the middle age of a quote, followed by a large spike of volume right as the quote begins to change.

Not only does this pattern remain consistent, but the relative contribution of each stage of a quote’s life to total volume remains consistent as well. For example, come rain or shine in the market, about 30% of the day’s volume comes as the quote changes to a new level. But as quotes change, prices become more directional separating winners from losers. This accelerates on ‘big move’ days.

What's a ‘big move? Let’s define it as the top and bottom deciles of intraday returns for single stocks and overnight returns for the S&P 500 respectively. Big days are characterized by higher volumes, but these higher volumes come with the added expense of wider spreads and faster moving quotes and that leads to higher mark-outs and less post trade quote-stability.

Discrete, timed matches on IntelligentCross helps place trades during the more stable mid-life of a quote, giving subscribers time to reload or take advantage of both spread-saving intraspread or midpoint liquidity.